In Part 1, we looked at the

Profit & Loss statement to answer the question: "Am I making money?"

That’s a great start, but it’s only half the story. The uncomfortable truth is that you can make a big profit on paper and still go bust if you can't pay the wages … or the rent … or whatever.

Welcome to Part 2 of our Jargon Buster. If the first article was about

performance, this one is about

survival.

Here, we look at the Balance Sheet and Cash Flow Statement. These reveal the true health of your business: what you own, what you owe, and whether you have enough fuel in the tank (cash) to keep the engine running.

This is where we decode terms like "Working Capital," "Liquidity," and "Equity." They might sound like dry textbook theory, but they’re actually the vital metrics that answer the scary question:

"Will I survive the year?"

Let’s clear away the fog so you can look beyond the sales figures and ensure your business is built on solid ground.

THE BALANCE SHEET

A balance sheet is a document showing a company's financial health at a point in time through the assets, liabilities and equity.

There are three parts to a Balance Sheet:

- Assets - This is the "positive" side of the balance sheet, divided into Fixed Assets and Current Assets

- Liabilities - This is the "negative" side of the Balance Sheet and shows the company's debts.

- Equity - This is the value of the investment made by the company's owners.

It is calculated by subtracting liabilities from assets.

If a company has traded profitably for some time, the equity value will likely be positive. But it is possible for unprofitable trading to produce negative equity – and here, the company will be kept going through loans and (perhaps) high trading debts.

Trial Balance

A Trial Balance is used to prepare accounts, where transactions are posted into different ledger categories (or types) in your accounts.

You'll have Sales, Purchases, and so on.

You will probably break these down further, with sales split down into (say) product types or geographical regions.

A Trial Balance lists every ledger item with its associated debit or credit balance.

So if you're an accountancy firm, all transactions that record consultancy fees will go into the relevant ledger item. And those that record bookkeeping services will go into another.

In this way, you build up a profile of how the business works.

In keeping with the traditional practice of

double entry bookkeeping, the total of debits must always equal the total of credits – so they balance.

If you use a competent accounting system (or bookkeeper…), this will always be the case.

ASSETS

This is

what you own, and falls into two sections: Fixed (long term) Assets and Current Assets.

Fixed Assets

These are things that a company owns that have value.

There are two main types:

- Tangible Assets - These are physical assets like vehicles, equipment and property.

Their cost is spread over time, using Depreciation.

- Intangible Assets - These are non-physical assets like intellectual property or goodwill.

Their cost is spread over time, using Amortization.

Both Depreciation and Amortization are used to align cost with the useful life of an asset.

Current Assets

These assets can quickly be turned into cash, usually within a year.

They include the following:

- Cash reserves - The amount of available cash held by a company, usually in bank accounts, but some may be in cash.

- Debtors (Accounts Receivable) - People (usually customers) who owe money to the company

- Inventory (or Stocks) - Merchandise or raw materials held in stock

- Prepayments - Payments made in advance for goods and/or services related to a future accounting period

LIABILITIES

Basically, this is

what you owe, and it has two components: Current Liabilities and Long Term Liabilities.

Current Liabilities

These are debts that a company owes with a short-term repayment (usually less than a year).

They include:

- Creditors (Accounts Payable) - People (usually suppliers) to whom the company owes money

- Accruals - Payments due (i.e., not yet made) for goods and/or services used in the current accounting period

- Loans - Examples are short-term loans, overdrafts and credit card balances

Long-Term Liabilities (Non-Current Liabilities)

These are debts that you do

not have to pay back within the next 12 months.

Examples would be multi-year bank loans, mortgages on property, or long-term finance leases for machinery.

Though they can be loans from a director, shareholder or other stakeholder.

If you'd like to learn more about accounts and finance, why not take a look at how we can help?

Boost your understanding of accounts with our online courses.

RRP $65 – limited time offer just

$23.99

EQUITY

This is the value of the business that belongs to the owners. Put simply, it represents what would be left over if you sold all your Assets and paid off all your Liabilities. But finding a buyer who will pay this theoretical value is usually a whole new ball game!

Anyway, it has two major components:

- Share Capital - This is the money invested into the company by the owners (shareholders) in exchange for shares.

It's the actual cash you (or the shareholders) have injected into the business.

Unlike a loan, this money does not need to be paid back. It stays in the business permanently.

So if you set up your company and put $100 into the bank account in exchange for 100 shares, your Share Capital is $100.

- Retained Earnings - This is the total amount of Net Profit the business has accumulated over its entire life, less any money paid out to shareholders (Dividends).

Think of it as the business’s "savings account" where profits have not been paid out (yet...)

Note: If this number is negative, it means the business has made more losses than profits over its lifetime. But contrary to a common belief, this does not mean that in practical terms a business is necessarily insolvent: it may have loans or preferential payment terms that enable it to continue trading./li>

CASH FLOW AND SURVIVAL METRICS

Cash Flow Statement

A cash flow statement records cash spent and received in an accounting period, monitoring the ongoing balance.

Cash flow is vitally important to a business, but it is not a measure of profit because it just looks at what you have in the bank (or safe?)

So you may have half a million in the bank, but it may all be owed to suppliers who are screaming at your door.

Or looking at it the other way, you may be generating huge profits, but your customers won't pay you so you can't pay your bills...

Profit vs. Cash Flow

Profit is a theory; Cash is a reality. This is the single most important distinction in business survival!

Profit is an accounting calculation. It creates a picture of financial success based on the invoices you have sent and the bills you have received.

But under accrual accounting, you record "Profit" the moment you send an invoice, even if the customer hasn't paid you yet. As we always say, you can be "profitable" on paper while having nothing in the bank!

Cash Flow is the actual movement of money in and out of your bank account.

The Reality: You cannot pay staff or rent with "Profit"; you can only pay with Cash.

The danger zone is the time gap between making the sale (Profit) and getting paid (Cash Flow).

Example: You sell £10,000 of goods in January. Your Profit & Loss says you had a great month! But if the customer pays in March, you have to survive January and February with no money coming in. And there are SO MANY business owners and managers who don't appreciate this simple fact of business life!

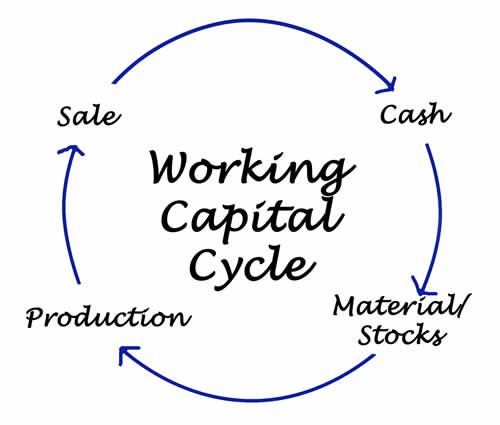

Working Capital

Working Capital is the money available to fund your day-to-day operations. It’s calculated by subtracting

Current Liabilities (bills you have to pay soon) from

Current Assets (cash you have or money owed to you).

Think of it as the fuel in your car's tank. You might have a powerful engine (High Profit), but if you run out of fuel (Working Capital), the car stops. A business can be profitable but still fail if it runs out of the working capital it needs to pay staff or suppliers while waiting for customers to settle their invoices.

Liquidity

Liquidity is a more focused view of your position. It doesn't just compare assets with liabilities, but it looks at how quickly and easily an asset can be converted into actual cash without losing value.

If your Working Capital position is poor (and people are chasing you for money) you need to take a quick look at your liquidity.

- High Liquidity: Cash in the bank is the ultimate liquid asset because you can spend it right away.

- Medium Liquidity: Inventory (Stock) is less liquid because you have to find a buyer first. And some stock items are a whole lot more saleable than others!

- Low Liquidity: Fixed Assets like buildings or heavy machinery are "illiquid." It could take months to sell them – often at a big discount if you need the money soon – to raise funds.

Why it matters: A business can have lots of current assets, but if they are predominantly tied up in stock, or unpaid customer invoices (Debtors), that's what is called "cash poor" and the business is vulnerable, even if its Balance Sheet looks impressive.

Break-Even Point

Break-Even Point is the exact moment where your total sales equal your total costs. At this point, the business makes no profit, but it also makes no loss. Knowing your break-even point is vital because every sale

after this point contributes directly to profit. And if sales fall below this point, you're losing money.

It helps you answer the question: "How much do I need to sell just to keep the lights on?"

Insolvency

This is the big one, because it's subject to a number of misconceptions.

Insolvency is the state where a business cannot meet its financial obligations, but there are two very different types.

- Balance Sheet Insolvency (Technical Insolvency): This means your total Liabilities are greater than your total Assets. You owe more than you own.

- Cash Flow Insolvency: This means you cannot pay your bills when they fall due.

The Critical Distinction is this. Being

Technically Insolvent is

not necessarily an offence. Many startups and rapidly growing companies technically owe more than they own but have enough cash coming in (or financed by loans) to pay every bill on time.

However, if you are

Cash Flow Insolvent (you cannot pay your staff or suppliers on time), you are in dangerous territory. And if you continue to trade while knowing you cannot pay your debts, you may be breaking the law (it's called wrongful trading).

If you business is in trouble, and you genuinely believe that it has a good chance of pulling through, put together a plan ... based on facts and likely outcomes, not hope. If you can secure finance to get the pressure off it should make sense to do so. But don't go too far! There are many, many examples of people who have over-committed, only to see their businesses fail, causing even more problems than they had before.

THE BOTTOM LINE

If you've made it this far, give yourself a pat on the back. You have successfully navigated the two scariest documents in business: the P&L and the Balance Sheet.

In Part 1, we learned that

Profit is the scoreboard. But here in Part 2, we've learned that

Cash is the oxygen.

The biggest takeaway from this series?

Profit is theory; Cash is reality.

You now understand why a business can look wildly successful on paper but still hit the wall because it ran out of Working Capital. You know that "Assets" aren't just fancy equipment you own, but places where your cash gets tied up. It's easy to think of that all-powerful computer system, or the refurbishment of the office, and feel how morale will go up and motivation will soar. But take a look at your finances and ask yourself whether you can really afford these things!

You don't need to become an accountant to run a successful business. But you do need to be able to spot the warning signs of trouble ahead. If your "Current Liabilities" are creeping up higher than your "Current Assets," you know it is time to hit the brakes - regardless of what the sales figures may say.

So, the next time your accountant presents the year-end figures, don't just nod along. Check the Liquidity. Check the Reserves. You now speak the language - use it to keep your business safe.